GSTR-5 return must be filed by persons registered under GST as non-resident taxable persons. Non-resident taxable persons are persons who occasionally undertakes transactions involving supply of goods or services or both, whether as principal or agent or in any other capacity, but who has no fixed place of business or residence in India. All non-resident taxable persons are required to obtain GST registration and file GSTR-5 returns.

What is GSTR-5 filing?

GSTR-5 is a type of GST return that must be filed by persons registered under GST Act as non-resident taxable persons. GSTR-5 return can be filed through the GST Common Portal by the person authorised to comply with GST provisions.

What is the due date for filing GSTR-5 return?

GSTR-5 return must be filed every month, on or before the 20th day. The return filed in a month would contain details of inward and outward supplies transacted by the person in the previous month.

Also, GST registration for non-resident taxable persons are provided with an expiry date. Hence, the non-resident taxable person would be required to file a GSTR-5 filing, 7 days before expiry of GST registration.

The following illustration shows GST return due date for all GST filings in India:

GST Return Filing Due Dates

What details must be provided in GSTR-5 filing?

In GSTR-5 filing, the non-resident taxable person would be required to furnish the following information for a month.

Inputs/Capital goods received from Overseas (Import of goods).

Amendment in the details furnished in any earlier return.

Taxable outward supplies made to registered persons (including UIN holders).

Taxable outward inter-State supplies to un-registered persons where invoice value is more than Rs 2.5 lakh.

Taxable supplies (net of debit notes and credit notes) to unregistered persons.

Amendments to taxable outward supply details furnished in returns for earlier tax periods.

Amendments to taxable outward supplies to unregistered persons furnished in returns for Earlier tax periods.

Total tax liability.

Tax payable and paid.

Interest, late fee and any other amount payable and paid.

Refund claimed from electronic cash ledger.

Debit entries in electronic cash/credit ledger for tax/interest payment [to be populated after payment of tax and submissions of return].

How to file GSTR-5 filing?

GSTR-5 return can be filed on the GST Common Portal using the user id and password provided during GST registration. For ease of compliance, GST software like LEDGERS can be used to file the returns automatically based on invoices and expenditures incurred during a month.

GSTR-5 return must be digitally signed with the digital signature of the authorised signatory. It’s important to note that all non-resident taxable persons are required to appoint an authorised person, resident in India as in-charge for GST compliance. Such an authorised signatory appointed for GST compliance can sign and file GSTR-5 return.

What is the penalty for late filing of GSTR-5?

GSTR-5 return must be filed on or before the 20th of each month. Unlike normal taxpayers, non-resident taxable persons are required to file only one return every month. For delay in filing a GSTR-5 return, a penalty of Rs.100 per day can be levied upto Rs.5000, for each return filed late.

GSTR-3 is a type of GST return that must be filed by regular taxpayers on the 20th of every month. GSTR-3 filing can be made on the GST Common Portal after filing GSTR-1 and GSTR- 2 for the month. If GSTR-1 return is not filed, then GSTR-2 return cannot be filed. Hence, all regular taxpayers must file GST returns regularly every month starting with GSTR-1 filing, followed by GSTR-2 and GSTR-3 return filing. In this article, we look at GSTR-3 return filing in detail.

Who should file GSTR-3 returns?

GSTR-3 return must be filed by all regular taxpayers registered under GST. In India, any person undertaking taxable supply of goods and services over Rs.20 lakhs in most states are required to be registered under GST. In some special category states, the aggregate turnover limit has been fixed at Rs.10 lakhs.

In addition to the aggregate turnover criteria, some types of taxable persons under GST like casual taxable persons and non-resident taxable persons are required to mandatorily obtain GST registration, irrespective of annual turnover criteria. Casual taxable persons and non-resident taxable persons are not required to file GSTR-3 filing. GSTR-3 return must be filed by regular taxpayers only. (Check GST registration eligibility).

What details must be provided in GSTR-3 filing?

GSTR-3 return is filed after filing of GSTR-1 and GSTR-2 returns. Most of the information to be filed in GSTR-3 return will be auto-populated based on GSTR-1 and GSTR-2 filings. Only some of the information will have to be verified, edited or added by the taxpayer.

The following information in GSTR-3 filing will be auto-populated:

Turnover

Outward supplies

Inter-State supplies (Net Supply for the month)

Intra-State supplies (Net supply for the month)

Tax effect of amendments made in respect of outward supplies

Inward supplies attracting reverse charge including import of services (Net of advance adjustments)

Inward supplies on which tax is payable on reverse charge basis

Tax effect of amendments in respect of supplies attracting reverse charge

Input tax credit

ITC on inward taxable supplies, including imports and ITC received from ISD [Net of debit notes/credit notes]

Addition and reduction of amount in output tax for mismatch and other reasons

Total tax liability

Credit of TDS and TCS

Interest liability

Late Fee

The following information must be provided by the taxpayer for GSTR-3 filing:

Tax payable and paid

Interest, Late Fee and any other amount (other than tax) payable and paid

Refund claimed from Electronic cash ledger

Debit entries in electronic cash/Credit ledger for tax/interest payment

What is the due date for filing GSTR-3 return?

All regular taxpayers must file GSTR-3 return before the 20th of every month. Before filing GSTR-3 return, GSTR-1 and GSTR-2 return must be filed. If GSTR-1 and GSTR-2 return are not filed, the GST common portal will not allow the taxpayer to file GSTR-3 return. The due dates for filing of GST returns for regular taxpayers are as follows:

GST Return Filing Due Dates

What is the penalty for late filing of GSTR-3 return?

A penalty of Rs.100 per day upto a maximum of Rs.5000 can be levied for late filing of any GST return. If GSTR-3 return is not filed, a penalty of Rs.100 per day will be applicable. If GSTR-1 and GSTR-2 return are also not filed, then a penalty of Rs.300 per day would be applicable.

How to file GSTR-3 return?

GSTR-3 return can be filed online on the GST Common Portal. The taxpayer can login to their GST common portal account, verify the auto-populated information, edit and add other information to file the return. GSTR-3 return must be digitally signed by the authorised person mentioned on the GST account. You can also file GST return through LEDGERS GST Software online.

GSTR-9 Filing – GST Annual Return – Due on 31st December

GSTR-9 or GST Annual Return must be filed by all regular taxpayers registered under GST. The only category of GST registered entities not required to file GSTR-9 filing are input service distributors, casual taxable persons and non-resident taxable persons. The due date for filing GSTR-9 is 31st December. In this article, we look at GSTR-9 filing in detail.

What is GSTR-9 Filing?

GSTR-9 or GST annual return is a type of GST return that must be filed by regular taxpayers and persons registered under GST composition scheme. GSTR-9 must be filed each year through the GST Common Portal or LEDGERS GST Sofware or at a GST Facilitation Centre.

Who should file GSTR-9A return?

Regular GST taxpayers filing GSTR-1, GSTR-2 and GSTR-3 must file GSTR-9A on or before 31st December, consolidating information furnished during the previous financial year.

Who should file GSTR-9B return?

GSTR-9B return should be filed by electronic commerce operators who are required to collect tax at source. In addition to GSTR-9B return, electronic commerce operators will also be required to file GSTR-8 return, every month.

Who should file GSTR-9C return?

Regular taxpayers registered under GST having an annual aggregate turnover of over Rs.2 crores during a financial year are required to get their accounts audited and file a copy of the audited annual account and reconciliation statement along with GSTR-9C return. The GST annual audit can be done by a practising Chartered Accountant or Cost Accountant.

What information should be filed in GSTR-9 return?

The following information is expected to be filed in GSTR-9A return:

Total value of purchases on which ITC availed (inter-State)

Total value of purchases on which ITC availed (intra-State)

Total value of purchases on which ITC availed (Imports)

Other Purchases on which no ITC availed

Sales Returns

Other Expenditure (Expenditure other than purchases)

Total value of supplies on which GST paid (inter-State Supplies)

Total value of supplies on which GST Paid (intra-State Supplies)

Total value of supplies on which GST Paid (Exports)

Total value of supplies on which no GST Paid (Exports)

Value of Other Supplies on which no GST paid

Purchase Returns

Other Income (Income other than from supplies)

Return reconciliation Statement

Arrears (Audit/Assessment etc.)

Refunds

Turnover Details

Profit as Per the Profit and Loss Statemen

Gross Profit

Profit after Tax

Net Profit

Details of Statutory Audit

What is the due date for filing GSTR-9 return?

GSTR-9 return or GST annual return is due on 31st December for all persons registered under GST. If an audit is required for GSTR- filing, then the details of audited statements must also be filed before 31st December in GSTR-9C.

The due dates for all types of GST return in India are as follows:

GST Return Filing Due Dates

What is the penalty for late filing of GSTR-9 return?

A per day penalty of Rs.100, up to a maximum amount of Rs.5000 would be applicable for late filing of GSTR-9 return. Only if all the GSTR-1, GSTR-2 and GSTR-3 returns are filed, the taxpayer would be able to file GSTR-9 return on the GST Portal.

Should GSTR-9 return be audited?

Yes. Regular taxpayers registered under GST having an annual aggregate turnover of over Rs.2 crores during a financial year are required to f the GSTR-9 return with audited accounts. GSTR-9 accounts can be audited by a practising Chartered Accountant or Cost Accountant.

Any person having GST registration can claim a refund under the GST Act for tax, interest, penalty, fees or any other amount paid by him using FORM GST RDS-01. GST RDS-01 form can be filed on the GST common portal. Along with Form GST RFD-01, various documents must be provided as evidence in the Annexure. We look at such documents required for GST refund in this article.

Documents Required for GST Refund

All GST refund application must contain the following documents attached as annexures to Form GST RDS-01:

Refund Passed by GST Officer or Tribunal

In case a refund application is made based on the orders by a GST officer or Appellate or Tribunal, then the reference number of the order and a copy of the order passed resulting in a refund or reference number of the payment claimed as refund should be attached.

In case of refund due to provisional assessment, the reference number of the final assessment order and a copy of the order should be attached.

Refund for Exports

In case of refund applications made on account of export of goods, a statement containing the number and date of shipping bills or bills of export and the number and the date of the relevant export invoices should be attached.

In case of refund on account of export of services, a statement containing the number and date of invoices and the relevant Bank Realisation Certificates or Foreign Inward Remittance Certificates should be attached.

In case of deemed exports, a statement containing the number and date of invoices along with such other evidence should be attached.

For refund applications made on account of supply of goods to a Special Economic Zone unit or SEZ developer, a statement containing the number and date of invoices along with the evidence regarding the endorsement should be attached.

In case of supply of services to a SEZ, a statement containing the number and date of invoices, the evidence regarding the endorsement along with the proof should be attached.

In case of refund application made on account of supply of goods or services made to a Special Economic Zone unit or a Special Economic Zone, declaration to the effect that the Special Economic Zone unit or the Special Economic Zone developer has not availed the input tax credit of the tax paid by the supplier of goods or services should be attached.

Excess Payment of Tax

Refund applications made on account of excess payment of tax must include a statement showing the details of the amount of claim on account of excess payment.

For refund of unutilised input tax credit that has accumulated on account of the rate of tax on the inputs being higher than the rate of tax on output supplies, a statement containing the number and the date of the invoices received and issued during a tax period should be attached.

Statement showing the details of transactions considered as intra-State supply but which is subsequently held to be inter-State supply if refund is due to wrong classification.

GST Refund of Over Rs.2 Lakhs

For all GST refund over Rs.2 lakhs, a declaration to the effect that the incidence of tax, interest or any other amount claimed as refund has not been passed on to any other person must be submitted. Further, a Chartered Accountant or Cost Accountant Certificate in Annexure 2 should also be attached.

Place of supply concept under GST plays an important role in determining the applicability of IGST or CGST & SGST. Also, in the GST invoice and GST return filing, place of supply must be mentioned mandatorily. Hence, we look at the GST place of supply concept in detail in this article.

Inter-State vs Intra-State Supply

Place of supply dictates the type of supply, which determines the applicability of GST as under:

Intra-State Supply

Intra-state supply is the supply of goods or services within the same state or union territory. Hence, a supply of service by a Chartered Accountant firm in Tamil Nadu to a client in Tamil Nadu would be termed as intra-state supply. Intra-state supply attract CGST and SGST.

Inter-State Supply

Inter-state supply attracts IGST. Various types of transactions as under can be classified as inter-state supply:

Supply of goods or services from one State or Union Territory to another State or Union Territory.

Import of goods or services.

Export of goods or services.

Supply of goods or services to or by SEZ.

Supplies to international tourists.

Any other supply which cannot be treated as intra-state supply.

Place of Supply for Goods

Place of supply for goods is determined as follows:

For the supply of goods that involve transportation, place of supply would be the location of the delivery of goods to the recipient.

In case goods are delivered to the recipient on the direction of a third person, then the principal place of business of the third person would be the place of supply.

For example, if a designer orders 100 meters of fabric to be delivered to a Tailor for stitching, the principal place of business of the designers would be the place of supply of goods.

If a supply of goods does not involve transportation, then the place of supply would be the location of the goods at the time of delivery to the recipient.

For example, the clothing sold by a designer in a store at Tamil Nadu would have the place of supply mentioned as Tamil Nadu.

If goods are assembled or installed at a site, the place of supply would be the place of installation or assembly.

For goods sold on-board a vessel or vehicle, the place of supply would be the location where the goods were taken on board.

For goods imported into India, the location of the importer would be the place of supply. For goods exported from India, the place of supply would be a location outside of India.

Place of Supply for Services

The default method to be used for determining the place of supply for services is:

If the supply of service is made to a person registered under GST, then the location of the recipient would be the place of supply.

If a supply of service is made to a person not registered under GST, then the location of the recipient on record would be the place of supply. If the location of the recipient is not determinable, then the location of the supplier would be the place of supply.

Separate provisions have been provided in the IGST Act for determining the place of supply for various types of services like architect services, restaurants, transportation service and more. The above methodology is applicable only for supply of services for which provisions have not been provided for in the IGST Act.

GST Registration – Documents Requested or Application Rejected

All entities engaged in providing supply of more than Rs.20 lakhs of goods or services in most states are required to obtain GST registration (Check GST registration criteria). Once a GST registration is submitted on the GST Common Portal, GST registration certificate is provided to most applicants within a period of 10 working days. However, some applicants may be requested by the GST department to submit additional information or documents. In rare cases, the application for GST registration could also be denied. In this article, we look at such cases, wherein after submission of a GST registration application, additional documents are requested or the GST application is rejected.

Submission of GST registration application

After submission of a GST registration application along with the list of documents required, an acknowledgement as shown below is provided to the applicant.

Sample GST Registration Acknowledgement

The ARN number mentioned in the GST registration application acknowledgement can be used to track the status of the application. It normally takes about 7 working days for the provisional GSTIN to be provided and an additional 2 days for providing final GSTIN with GST registration certificate. If GST registration application is approved, GST registration certificate as shown below will be issued in soft-copy format to the applicant.

GST Registration Certificate Sample – Annexure A

Additional Documents Requested

If the GST registration application does not contain all the necessary documents or information, then the GST officer processing the application would issue a notice seeking additional information or clarification or documents as shown below:

Sample GST REG-03

In such a case, the GST registration applicant can submit the required information or documents as cited by the GST Officer on the common portal before the date mentioned in the notice. After submission of the information, if the GST Officer is satisfied with the information submitted, GST registration would be issued. In case, the processing officer is not satisfied with the reply or the applicant fails to submit a reply within the time mentioned, the application would be cancelled.

It is important to note that a GST Officer cannot order for a personal hearing for issuing a new GST registration certificate. The status of processing of the application and any concerns can be mentioned only through the provided GST forms.

GST Registration Application Rejected

In case, the processing officer is not satisfied with the reply or the applicant fails to submit a reply within the time mentioned, the application would be cancelled. On rejection of a GST registration application, the GST Officer would issue the following notice to the taxpayer. All GST application rejections must be conveyed to the applicant in writing along with the reasons for rejection, as per GST regulations.

GST Registration Application Rejection Order

If the taxpayer has rectified the issues mentioned in the GST registration application cancellation order, a fresh GST registration application can be submitted. In case the applicant has questions regarding the reasons for rejection, the nearest GST Seva Kendra can also be approached for assistance.

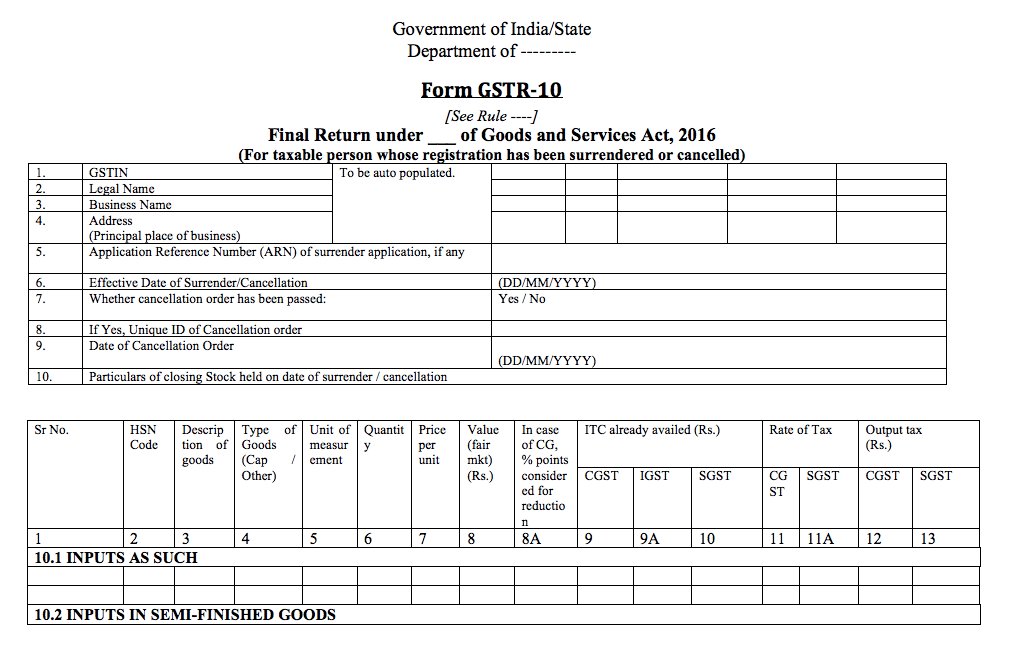

GSTR-10 Filing – Final GST Return Due on Cancellation

GSTR-10 is a type of GST return that must be filed by persons registered under GST – on cancellation or surrender of GST registration.

Who should file GST Return?

GSTR-10 should be filed on cancellation or surrender of a GST registration. Hence, regular taxpayers would not file GSTR-10. Only persons registered under GST who have applied for surrender or cancellation of GST registration.

What is the due date for filing GSTR-10?

GSTR-10 must be filed within 3 months of cancellation of GST registration. Hence, if a GST registration was cancelled on 1st January, then GSTR-10 return would be due on 31st March.

The chart below shows the due dates for all types of GST returns in India:

GST Return Filing Due Dates

What information should be provided in GSTR-10 return?

The following information must be provided in the final GST return:

GSTIN of the taxpayer

ARN of GST registration surrender application

Effective Date of GST registration surrender/cancellation (DD/MM/YYYY)

If GST cancellation order has been passed

Unique ID of cancellation order

Date of Cancellation Order (DD/MM/YYYY)

Closing Stock held on date of GST registration surrender or cancellation

Inputs in semi-finished goods

Inputs in finished goods

Input services

Captial goods

Amount of tax payable on closing stock

A sample GSTR-10 return is attached below:

Sample GSTR-10 Form

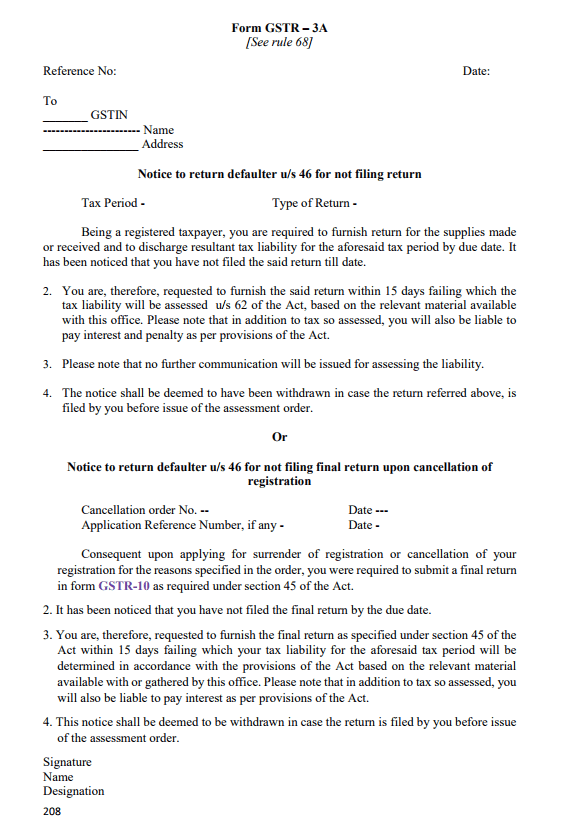

What is the penalty for not filing GSTR-10 return?

If a taxpayer fails to file final GST return return, then a notice for not filing final return upon cancellation of registration would be sent to the taxpayer as shown below:

Sample GSTR-3A

On sending the notice for not filing GSTR-10 return, the taxpayer would be provided a 15 days period for filing the return along with all the documents. If the taxpayer fails to respond to the tax notice or does not file the GSTR-10 return, then the tax officer would pass the final order of cancellation with the amount of GST tax payable along with interest or penalty.

Hence, to avoid unnecessary litigation or liabilities, it is important for all taxpayers who have surrendered or cancelled their GST registration to file GSTR-10 return within 3 months.

Talk to an IndiaFilings Advisor to Know more about GST Registration

Reversing Input Tax Credit – Non-payment of Invoice

GST invoices should be issued when goods or services have been delivered to the customer and payment is reasonably assured. On raising the tax invoice, the supplier would be required to disclose the sale in the monthly GSTR-1 filing and pay the GST tax payable to the Government, even if the customer has not made payment on the invoice.

In some cases, the customer of a goods or service might fail to make payment on the invoice. In such cases, the supplier can take the following steps to reverse the input tax credit enjoyed by the recipient without making payment.

Step 1: Intimate the Customer

Though the supplier is not required to provide any intimation to the customer before reversing input tax credit, it is a good practice to make a written request to the customer for making payment on the overdue-invoice.

Step 2: File GSTR-2

While filing the GSTR-2 return on or before the 15th of a month, the supplier can mention the details of invoices for which payment was not received along with GSTIN of the customer. To reverse input tax credit, the following information pertaining to the transaction must be provided in the GSTR-2 filing:

GSTIN of customer

Invoice number

Amount not paid

Amount of input tax credit availed

The above information must be filed in a GSTR-2 return within 180 days of the date of issue of invoice for reversal of input tax credit.

Step 3: Reversal of Input Tax Credit

On filing GSTR-2 return, the amount of input tax credit availed by the customer would be added to the output tax liability for the month in which the details are furnished. The customer would then be liable to pay interest for the wrongly availed input tax credit for a period starting from the date of availing credit till the date when the amount was added to the output tax liability.

Under GST Invoice Rules and Format, suppliers are required to mandatorily display the HSN code or SAC code of the goods or services supplied. However, in order to make compliance easier for small and medium sized enterprises, the requirement for disclosing HSN code on invoice has been relaxed. In this article, we look at the rules concerning display of HSN code on the invoice in detail.

What is HSN Code?

HSN Code is an internationally accepted goods classification system used in over 200 countries. Under the HSN code system, goods have been classified into 97 different chapters. HSN code consists of 6 digits.

The HSN code chapter is represented in the first two digits of the HSN code.

The heading of the goods is represented in the third and fourth digit of the HSN code.

The sub-heading of the goods is represented in the fifth and sixth digit of the HSN code.

With the HSN code acting as a universal classification for goods, the Indian Government has decided to adopt the use of HSN code for classification of goods under GST and levy of GST.

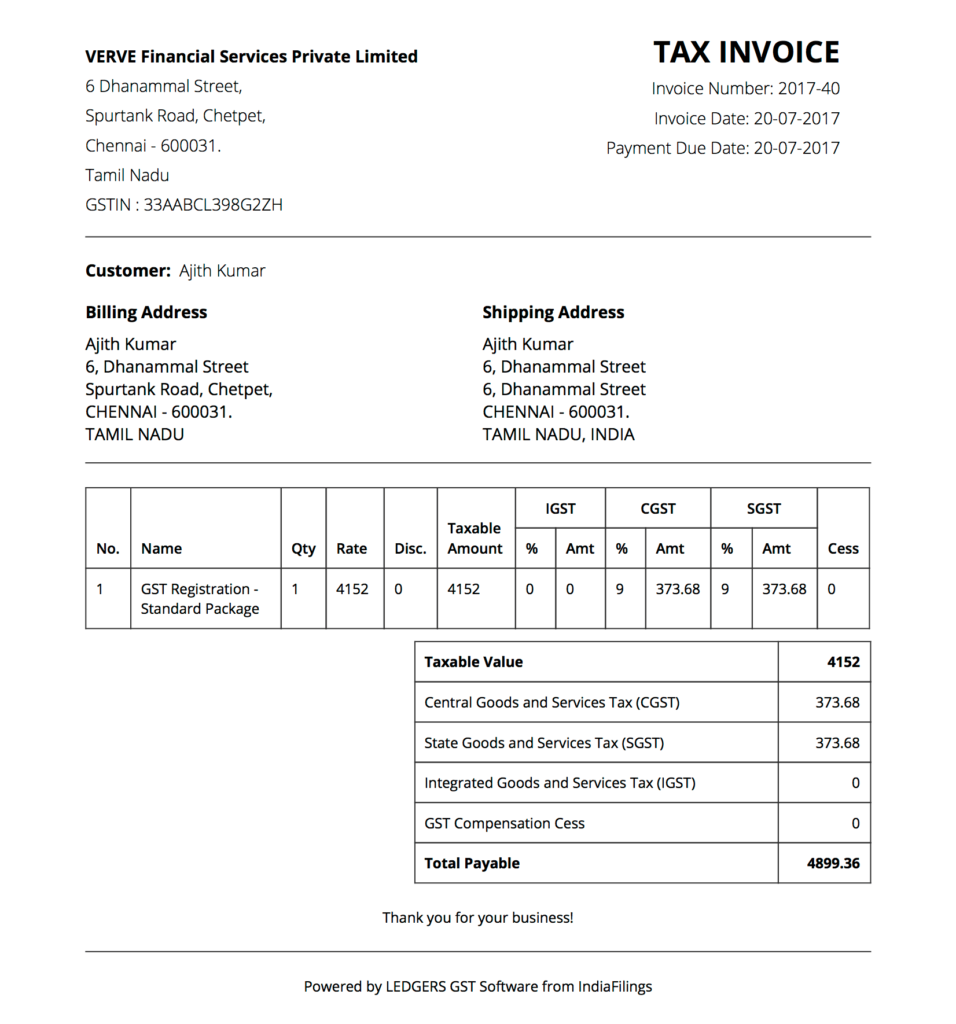

According to the GST rules and regulations, all suppliers of goods or services are required to issue a tax invoice mandatorily, when the value of supply is over Rs.200. The tax invoice issued under GST is required to contain the following information:

Name, address and GSTIN of the supplier.

Invoice number not exceeding sixteen characters.

Date of tax invoice.

Name, address and GSTIN of the customer, if available.

HSN code for goods or SAC code for services.

Description of goods or services.

Quantity supplied.

Total value of supply.

Taxable value of the supply.

Rate and amount of GST

Place of supply

A sample GST tax invoice is attached below:

Sample GST Invoice

HSN Code on Invoice

Many small businesses might find it cumbersome to find and update HSN code for the goods supplied. Hence, to reduce the compliance burden of small businesses, the GST Council has relaxed the requirement for displaying HSN code on invoices based on the sales turnover.

As per Notification No. 12/2017 – Central Tax dated 28th June, 2017, HSN code on the invoice can be displayed as follows:

Entities having less than Rs.1.5 crores annual turnover in the preceding financial year will not be required to display HSN code on the invoice.

Entities having Rs.1.5 crores to Rs.5 crores annual turnover in the preceding financial year will be required to display the first two digit (Chapter) of the HSN code on the invoice.

Entities having more than Rs.5 crores annual turnover in the preceding financial year will be required to display the first two digit (Chapter) and chapter heading of the HSN code on the invoice. Thus, only entities having more than Rs.5 crores of annual turnover would be required to display 4 digit HSN code on the invoice.

Regular taxpayers, casual taxable persons and non-resident taxable person who apply for GST registration are provided with GSTIN or Goods and Services Tax Identification Number. In addition to the GSTIN, GST Unique ID can be allotted by the GST Authorities. In this article, we look at GST Unique Id in detail.

GSTIN vs GST Unique ID

GSTIN or Goods and Services Tax Identification Number is allotted to regular taxpayers required to collect GST and file GST returns. On the other-hand, GST Unique ID is allotted only a certain class of persons notified in the GST Act. Hence, GSTIN and GST Unique ID are different forms of identification under GST.

Who can get GST Unique ID?

The GST Act states that any specialised agency of the United Nations Organisation or any Multilateral Financial Institution and Organisation notified under the United Nations (Privileges and Immunities) Act, 1947, Consulate or Embassy of foreign countries and any other persons notified by the Commissioner can be granted a GST Unique Identity Number. GST Unique Identity Number can be used for the purposes of claiming GST refund on notified supplies of goods or services and other purposes as notified by the GST authorities.

How to apply for GST UIN?

GST UIN can be granted to Consulates, Embassies and other specialised agencies as mentioned above. The application for GST UIN can be made in Form GST REG-13. GST REG-13 is shown below:

GST REG-13 – Page 1GST REG-13 – Page 2

In addition to applying for GST UIN using FORM REG-13 on the GST Common Portal, consulates and embassies can also be granted suo-moto registration by a GST officer.

How long does it take to obtain GST UIN?

After filing FORM GST REG-13, the GST office processing the application is required to issue a GST certificate in FORM GST REG-06 within a period of three working days from the date of the submission of the application.

GSTR-11 Filing

All persons having GST UIN are required to file a quarterly GSTR-11 return. Based on the GSTR-11 return filing, GST refunds will be processed by the Government. Further, UIN holders will not be allowed to add or modify any details in GSTR-11, only the auto-populated information from GSTR-1 filing can be verified and filed by the GST UIN holder. Know more about GST return filing.

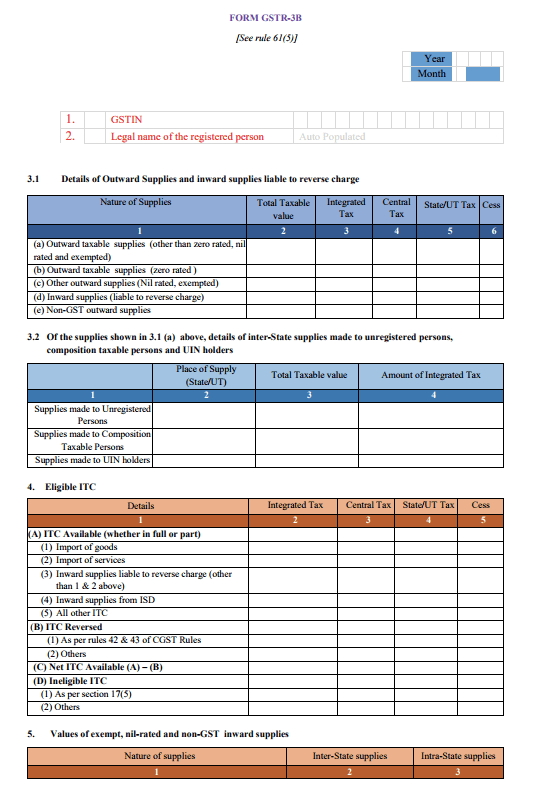

GSTR-3B return must be filed by all persons having GST registration in the month of August and September. GSTR-3B return is due on the 20th of August and September 2017. In this article, we look at GSTR-3B return filing in detail along procedure for filing online.

Who should file GSTR-3B return?

GSTR-3B return must be filed by all person registered under GST until the normal schedule for filing of GST return commences in the month of October 2017.

What is the due date for filing GSTR-3B return?

GSTR-3B return is due on the 20th of August and 20th of September 2017. From October 2017, the taxpayers would be required to file GSTR-1, GSTR-2 and GSTR-3, as per normal schedule. Hence, GSTR-3B is a temporary return that must be filed monthly until October, 2017.

What is the penalty for not filing GSTR-3B return?

The Government has mentioned that during the GST transition period, leniency would be shown to taxpayers to famliarize themselves with the GST provisions. Hence, no penalty has so far been announced for not filing GSTR-3B return. However, it is expected that taxpayers who fail to file GSTR-3B returns would be ineligible to being filing GSTR-1, GSTR-2 and GSTR-3 returns from the month of October. Failure to file GSRT-1, GSTR-2 and GSTR-3 returns will attract penalty of Rs.100 per day.

What details must be provided in GSTR-3B return?

GSTR-3B is a simplified GST return, in which outward supplies and inward supplies are not matched. Hence, the taxpayer while filing GSTR-3B return is required to furnish details of both outward supplies and inward supplies. The table below shows the details that must be submitted in GSTR-3B return.

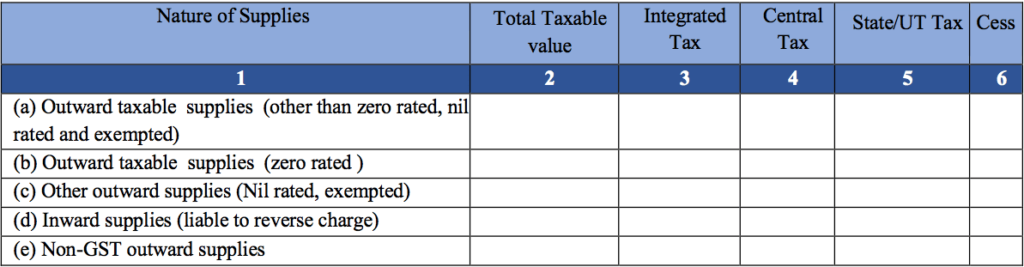

3.1 Details of outward supplies and inward supplies liable to reverse charge

Nature of Supplies

Total Taxable Value

Integrated Tax

Central Tax

State/UT Tax

Cesss

1

2

3

4

5

6

(a) Outward taxable supplies (other than zero rated, nil rated and exempted)

(b) Outward taxable supplies (zero rated )

(c) Other outward supplies (Nil rated, exempted)

(d) Inward supplies (liable to reverse charge)

(e) Non-GST outward supplies

Explanation: In the first table, details of both inward and outward supplies must be provided by the taxpayer. Also, all heads must be broken down into the categories of taxable value, IGST, CGST, SGST and Cess.

For example, if a taxpayer issued invoices worth Rs.1 lakhs in the month of July and collected Rs.18000 as IGST, then in row (a), total taxable value, Rs.1 lakh must be mentioned. The IGST of Rs.18000 collected must be mentioned in row (a) under the heading Integrated Tax.

Similarly, all zero rated supplies must be mentioned in row (b), NIL rated outward supplies must be mentioned in row (c), inward supplies wherein reverse charge is applicable must be mentioned in row (d) and Non-GST outward supplies must be mentioned in row(e).

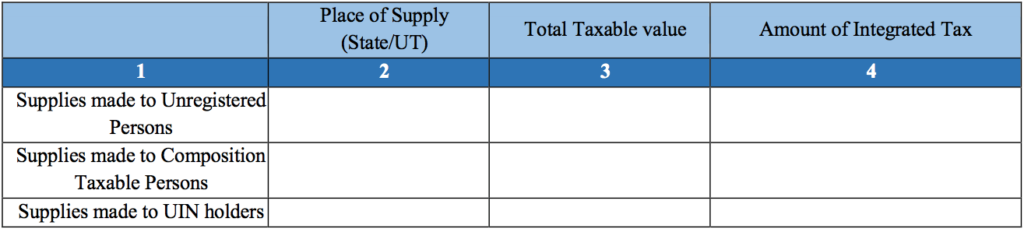

3.2 Of the supplies shown in 3.1 (a) above, details of inter-State supplies made to unregistered persons, composition taxable persons and UIN holders

Place of Supply (State/UT)

Total Taxable value

Amount of Integrated Tax

Supplies made to Unregistered Persons

Supplies made to Composition Taxable Persons

Supplies made to UIN holders

Explanation: In the second table, details of supplies already listed in 3.1 (a) is further broken down. This table would be applicable only if the taxpayer made taxable supplies to unregistered persons, composition taxable persons or UIN holders.

For supplies made to unregistered persons, the total taxable value and amount of integrated tax collected must be provided for by place of supply or State. The same breakup must also be provided for supplies made to composition taxable persons and UIN holders. UIN is provided to embassies, consulates and UN bodies.

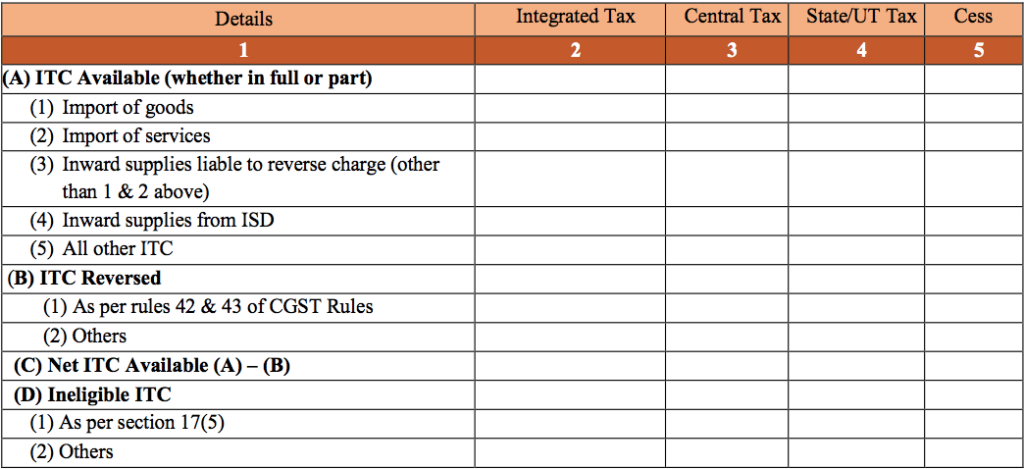

4. Eligible Input Tax Credit (ITC)

Integrated Tax

Central Tax

State/UT Tax

Cess

(A) ITC Available (whether in full or part)

(1) Import of goods

(2) Import of services

(3) Inward supplies liable to reverse charge (other than 1 & 2 above)

(4) Inward supplies from ISD

(5) All other ITC

(B) ITC Reversed

(1) As per rules 42 & 43 of CGST Rules

(2) Others

(C) Net ITC Available (A) – (B)

(D) Ineligible ITC

(1) As per section 17(5)

(2) Others

Explanation: In this table, the taxpayer must provide details of all eligible input tax credit. In part (A), the taxpayer should provide details of input tax credit available with the breakup of IGST, CGST, SGST and Cess. In addition, details of eligible input tax credit must be provided under the following heads:

Import of goods

Import of services

Inward supplies liable to reverse charge (other than 1 & 2 above)

Inward supplies from ISD

All other Input tax credit available

Input Tax Credit Reversed: Rule 42 of the CGST rules pertain to the procedure for determination of input tax credit on inputs or input services and input tax credit reversal. This section would be applicable for inputs being partly used for the purposes of business and partly for other purposes, or partly used for effecting taxable supplies including zero rated supplies and partly for effecting exempt supplies.

Rule 43 of the CGST rules pertain to the manner of determination of input tax credit for capital goods. This section would be applicable for the taxpayer claiming input tax credit on capital goods, which are being partly used for the purposes of business and partly for other purposes, or partly used for effecting taxable supplies including zero rated supplies and partly for effecting exempt supplies.

Net Input Tax Credit Available: By netting-off, the available input tax credit and input tax credit reversed, the taxpayer would arrive at net input tax credit available.

Ineligible Input Tax Credit: For certain items like transportation of goods, health club memberships, travel benefits extended to employees and food, input tax credit cannot be claimed. All such ineligible input tax credit under Section 17(5) of the CGST Act and other notification must be listed.

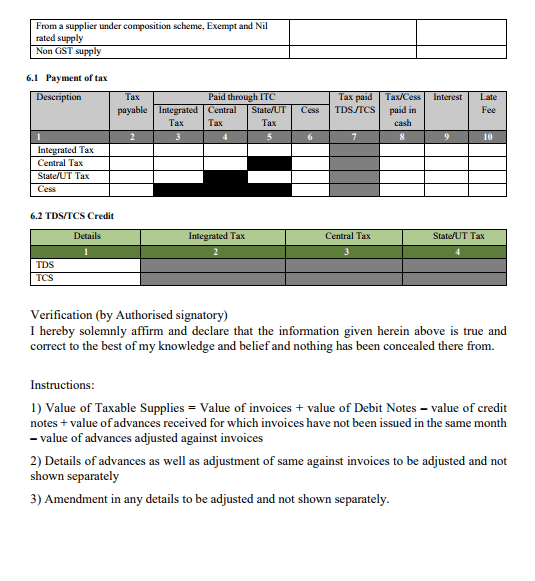

5. Values of exempt, nil-rated and non-GST inward supplies

Nature of Supplies

Inter-State Supplies

Intra-State Supplies

From a supplier under composition scheme, Exempt and Nil rated supply

Non GST supply

Explanation: In this table, value of inward supplies that are nil-rated or non-GST inward supplies received by the taxpayer must be mentioned.

6.1 Payment of tax

Description

Tax Payable

ITC Claim Integrated Tax

ITC Claim

Central Tax

ITC Claim

State/UT Tax

Cess

Tax Paid

TDS/TCS

Tax/Cess

Paid in Cash

Interest

Late Fee

1

2

3

4

5

6

7

8

9

10

Integrated Tax

NA

Central Tax

NA

NA

State/UT Tax

NA

NA

Cess

NA

NA

NA

NA

Explanation: In this table, details of GST paid by the taxpayer must be mentioned with the breakup of IGST, CGST, SGST and Cess. Since TDS and TCS provisions have not been implemented, column 7 need not be filled-in. In column 3, 4 and 5, the taxpayer can set-off GST liability with available input tax credit. ince SGST input tax credit

Since SGST input tax credit cannot be used for CGST payment, the cell is listed as NA. Similarly, CGST input tax credit cannot be used for SGST payment and the cell is listed as NA.

6.2 TDS/TCS Credit

Details

Integrated Tax

Central Tax

State/UT Tax

TDS

NA

NA

NA

TCS

NA

NA

NA

Explanation: In this table, details of TDS and TCS credit available with the taxpayer is listed. As mentioned above, since TDS or TCS provisions have not been implemented, this table need not be completed.

GSTR-3B Return

A sample GSTR-3B return is reproduced below for reference:

GSTR-3B Return FormatGSTR-3B Return Format – Page 2

How to file GSTR-3B Return?

GSTR-3B return can be filed online through the GST Common Portal or using LEDGERS GST Software. Based on the invoices raised and purchases invoices recorded, GSTR-3B return can be prepared easily.

In GST, the terms interstate and intrastate have tremendous significance in the determination of IGST, CGST or SGST. Interstate supply attracts IGST, while intrastate supply attracts CGST and SGST. In this article, we look at the definition of interstate supply and intrastate supply as per GST Act.

What is Interstate Supply?

Under GST, supply of goods or services from one state to another would be called as interstate supply. The GST Act defines interstate supply as when the location of the supplier and the place of supply for the customer are in:

Two different States; or

Two different Union territories; or

State and a Union territory.

In addition to the above, the supply of goods imported into India, till they cross the customs station is also classified as interstate supply. Also, supply of goods or services to or by a Special Economic Zone developer or a Special Economic Zone unit is classified as interstate supply.

What is Intrastate Supply?

Under GST, supply of goods or services within the same state or Union territory is called as intrastate supply. However, supply of goods or services to a Special Economic Zone developer or Special Economic Zone unit situated within the same state would not be intrastate supply. As any supply of goods or services to a Special Economic Zone developer or Special Economic Zone unit is classified as intrestate supply.

GST Interstate vs Intrastate Supply

GST Interstate vs Intrastate Supply

Under GST, interstate supply attracts Integrated Goods and Services Tax or IGST. Intrastate supply attracts both Central Goods and Services Tax (CGST) and State Goods and Services Tax (SGST). In the case of intrastate supply, the GST rate for the goods or services would remain the same. However, the GST rate and tax amount are divided equally into the two heads namely SGST and CGST.

For example, if a Rs.1,00,000 worth laptop is sold by an electronics store in Maharashtra to a customer in Karnataka and the applicable GST rate is 18%, then Rs.18000 IGST would be applicable. If the laptop is sold by an electronics store in Maharashtra to a customer in Maharashtra, then CGST or Rs.9000 and SGST or Rs.9000 would be applicable.

GST Registration Check – How to Check GSTIN Validity?

GST registration is mandatory in most states for businesses having an aggregate annual turnover of more than Rs.20 lakhs per year. In addition to the aggregate turnover criteria, businesses involved in import or export, interstate supply, ecommerce and other such conditions are required to obtain GST registration mandatorily irrespective of annual aggregate turnover. In this article, we look at the procedure for checking GST registration validity in detail.

GST Registration Validity

GST registration for regular taxpayers do not have an expiry date and is valid until it is surrendered or cancelled. Only the GST registration for non-resident taxable persons and casual taxable persons are valid until the date mentioned on the GST registration certificate.

How to Check GST Registration Application Status

If you have applied for GST registration, it normally takes about 7 working days for the provisional GSTIN to be allotted and 10 days to obtain the final GSTIN with GST registration certificate. From the time of submission of GST registration application, the status can be checked on the GST portal.

You can follow the below steps to find the status of a GST Registration application:

Enter the ARN number of GST registration application in the place provided and complete the CAPTCHA.

Step 3: GST Registration Application Status

On clicking search, the GST registration application status is shown as below. If the GST registration application is approved, the message approved will be displayed next to the status.

GST Registration Application Status

How to Check Existing GST Registration Status

In case you would like to check the status or validity of an existing GST registration, then the following steps can be used.

Step 1: Go to GST Portal

Visit the GST Portal. You can also go to gst.gov.in and select Services -> User Services -> Search Taxpayer.

GST Registration Status Check

Step 2: Enter the GSTIN Number

Enter the GSTIN number of the supplier or customer in the place provided and complete the CAPTCHA.

Step 3: GST Registration Application Status

On clicking search, the GST registration status is shown as below along with the status of registration.

GST Registration Status

In case you require GST registration for your business, visit IndiaFilings or get in touch with an IndiaFilings Advisor.

Composite Supply & Mixed Supply Accounting under GST

The GST Council has clearly provided GST rates for all goods and services. For most goods and services, the GST rates based on HSN code or SAC code would be applicable and the GST to be paid by the customer can be easily ascertained. However, in some supplies, the supply will consist of a combination of services or combination of goods or both which attract different GST rates, making GST tax calculation more complex. In such cases, the procedure laid down in the GST Act on accounting for composite supplies or mixed supplies can be used.

What is a Composite Supply?

A composite supply under GST means the supply consists of two or more taxable supplies of goods or services which are naturally bundled and supplied together in the ordinary course of business, one of which is a principal supply.

For example, in the supply of an ice cream, the supplier provides both ice cream an eatable and a plastic spoon for consuming the ice cream. The GST rates and HSN code for ice cream and plastic spoon are very different. However, with the concept of composite supply, ice cream will be held as principal supply and the GST rate applicable for ice cream can be applied for the entire supply.

GST Rate for Composite Supply

The GST rate applicable for a composite supply transaction can be determined based on the following manner:

If a composite supply consists of two or more supplies, one of which is a principal supply, then the supply should be taxed similar to the principal supply.

So in the case of the ice cream example, the principal supply would be ice cream as it is the principal supply in the transaction.

What is Mixed Supply?

Under GST, a mixed supply means two or more individual supplies of goods or services are made in conjunction with each other for a single price and the supply cannot be classified as a composite supply. The major difference between mixed supply and composite supply would be if the items are supplied together in the ordinary course of business.

In the example for composite supply, ice cream and plastic spoon were cited and bundling of those items is a normal trade practice. However, an example for mixed supply would be bundling of sweets, dry fruits, juices, clothes and crackers in a single package supplied for a single price. In this example, the bundling of sweets, dry fruits, juices, clothes and crackers are not an ordinary trade practice and can be held as mixed supply.

GST Rate for Mixed Supply

If a supply cannot be classified as a composite supply, then it must be treated as mixed supply. In case of mixed supply, the highest GST rate of the items in the bundle must be adopted as the GST rate for the entire supply.

Thus, in the above example of sweets, dry fruits, juices, clothes and crackers; if crackers attract 28% GST rate, then the 28% rate would be applied to the entire bundle.

India is a nation of farmers with the agriculture sector contributing a large chunk of the economy. Small scale agriculture has been exempt under GST and most of the basic produce sold in fresh form do not attract any GST. However, GST registration and GST compliance may be mandatory for large scale farmers and companies involved in agriculture. In this article, we look at the taxation of agriculture under GST in detail.

Is GST Applicable for Agriculture?

According to the GST Act, only an agriculturist, to the extent of supply of produce out of cultivation of land is exempt from GST registration requirement. Further, the Act goes on to define an agriculturist as an individual or a Hindu Undivided Family who undertakes cultivation of land:

By own labour, or

By the labour of family, or

By servants on wages payable in cash or kind or by hired labour under personal supervision or the personal supervision of any member of the family.

Hence, only small agriculturist would be exempt from GST compliance. Any person who operates a company or LLP or any other type of entity for the purpose of undertaking agriculture would be required to obtain GST registration if the aggregate turnover criteria or other GST registration criteria is satisfied and they sell goods that attract GST. (Check if GST registration is required)

Will Agriculturist Pay GST?

As the GST Act exempts only an agriculturist as defined above from GST, many involved in formal agriculture or agricultural business can be liable for registration, collection and compliance under GST. Since GST is a consumption based tax, any person involved in agricultural businesses and having GST registration would also be able to take input tax credit on GST paid and pass on the ultimate GST liability to the end consumer.

On the other hand, an agriculturist as per GST Act not having GST registration would not be required to comply with GST requirements. However, an agriculturist would still have to pay GST on purchases which attract GST tax. For example, 12% GST rate is applicable on items like water pump, milking machines and self-unloading trailers used for agricultural purposes. Hence, an agriculturist would be making GST payment while purchasing such goods or services which attract GST.

GST Rates Applicable for Agriculture

Vegetables and produce from agriculture, including dairy, served fresh without any processing have been exempt from GST. Under GST, any person who is engaged exclusively in the business of supplying goods or services or both that are not liable to tax or wholly exempt from GST is not required to obtain GST registration.

Hence, even a formal farmer selling fresh produce would be exempt from GST registration or compliance, as he/she would fall under the category of a person engaged exclusively in the business of supplying goods that are not liable to tax or wholly exempt from GST.

GST Rate for Seeds & Fertilisers

Seeds and fertilisers are a major input for agriculturist and farmers. Both seeds and fertilisers are exempt from GST. Hence, agriculturists would not have to pay GST tax on their major input.

GSTR 3B Return must be filed all persons having GST registration before 20th August and 20th September. Once GSTR 3B returns are filed in August and September, the normal filing of GSTR-1, GSTR-2 and GSTR-3 will begin from October 10th. In this article, we look at the procedure for filing GSTR 3B return on the GST Common Portal.

Information Preparation

Before filing GSTR 3B return on the GST portal, the taxpayer must prepare the following information. As offline tool or API access has not been provided by the Government for filing GSTR 3B Return, the only way to file GSTR 3B is through the Government Portal.

Step 1: Prepare details of outward taxable supplies

GSTR 3B Details of Outward Supplies

In the first table, details of outward supplies and inward supplies liable to reverse charge must be provided. You can prepare this information by compiling details from all sales invoices issued during the month of July for GSTR 3B return due in August. In case you are using LEDGERS GST software, this information will be auto-populated for you.

Outward taxable supplies (other than zero rated, nil rated and exempted)

In this row, you will have to provide information about all invoices issued by the company that is NOT zero rated, nil rated and exempted. Hence, this row will contain details of all invoices for which GST was levied. The information about GST must be broken down further into taxable value, integrated tax, central tax, state tax and cess.

In the field for taxable value, mention the total bill amount. If IGST was payable on the taxable value, mention the same in the field for integrated tax. If CGST and SGST was applicable, it must be mentioned in the fields for central tax and state tax. Finally, if any cess was applicable, it must be mentioned in the GST cess field.

Important: The supplier is liable for payment of GST on the issuance of invoice, so the fields need to be completed based on the invoices issued and not based on payment received.

Outward taxable supplies (zero rated )

Exports and sales to SEZ units are zero rated. Hence, in this row details relating to exports and supplies made to SEZ units must be mentioned. As mentioned above, the details must be categorised by taxable value, integrated tax, central tax and cess.

Other outward supplies (Nil rated, exempted)

In this field, Nil rated and exempted supplies must be mentioned. Hence, goods or services which attract nil or 0% GST rate should be mentioned. As IGST, CGST and SGST component are not be applicable for exempt supplies, it would be zero, while the taxable value of such invoices issued must be mentioned.

Inward supplies (liable to reverse charge)

In this row, details of all inward supplies for which the business is liable to pay GST must be mentioned. Inward supplies liable for reverse charge are transactions wherein the recipient of the supply is made liable for payment of GST. You can break down inward supplies liable for reverse charge by taxable amount, integrated tax, central tax, state tax and cess.

Non-GST outward supplies

Some goods like petroleum crude, motor spirit (petrol), high speed diesel, natural gas and aviation turbine fuel have been kept out of GST. Details of outward supplies of such goods must be mentioned in this row with details of taxable amount.

Step 2: Prepare supplies to unregistered persons, composition dealers and UIN holders

GSTR 3B – Supplies made to unregistered persons

Supplies made to Unregistered Persons

In this table, inter-state supplies made to unregistered persons must be provided. Hence, aggregate level details of all B2C transactions would be listed here. As this table is a breakup of supplies shown in the above table, the value in the first table would always be higher.

In supplies made to unregistered persons, the amount of taxable value and integrated tax must be mentioned by State. Based on the number of states the taxpayer made supplies, the rows can be increased.

Supplies made to Composition Taxable Persons

In this table, supplies made to composition taxable persons must be mentioned along with state, taxable value and amount of integrated tax. Composition taxable persons are persons having GST registration but not eligible to collect GST.

Supplies made to UIN holders

UIN or GST Unique ID is provided to Consulates, Embassies and UN Bodies. In case the taxpayer made supplies to UIN holders outside of the state, such details must be provided in this row.

Important: This table contains details of inter-state supplies ONLY. Hence, only if supplies were made outside of the state, then information must be provided in this table. If all the supplies were intra-state, then this table would be filled with zeros.

Step 3: Prepare details of input tax credit

Persons registered under GST are eligible to avail input tax credit under GST for setting off GST liability. To avail input tax credit, the taxpayer must properly enter purchases invoices and track expenditure. In LEDGERS, if you had updated all your purchase invoice details, the following table would be auto populated.

GSTR 3B Input Tax Credit Availed

Input Tax Credit Available from Import of Goods

Import of goods is subject to levy of IGST on import. Taxpayers registered under GST can claim input tax credit for IGST paid on imports. In this table, details of all import of goods for which GST under IGST, CGST, SGST and Cess paid along with customs duty must be mentioned.

Input Tax Credit Available from Import of Services

Import of services into India is also subject to levy of IGST. In this row, details of import of services for which IGST was paid must be mentioned.

Inward Supplies Liable to Reverse Charge

Some types of inward supplies like OIDAR services are liable for reverse charge, wherein the recipient of the goods or service is liable for payment of GST. Such inward supplies wherein the taxpayer is liable for payment of GST must be mentioned here.

Inward Supplies from ISD

In this row, input tax credit availed from input service distributors must be mentioned. Input service distributors can be setup by taxpayers to distribute input tax credit. This row would be applicable only for taxpayers who have registered as an input service distributor.

All Other Input Tax Credit

This row would have to be completed for most taxpayers who purchased or received invoices for goods and services during the month of July. Based on the purchases, the details of integrated tax, central tax, state tax and cess paid by the taxpayer must be provided. To complete this field, it is important to compile all invoices received and calculate the amount of GST tax paid in the month of July.

Input Tax Credit Reversed

Input tax credit cannot be availed fully for certain supplies which are used partly for business purpose and partly for other purposes. For such input tax credit must be reversed as per Rule 42 and Rule 43 of the CGST rules. Details of input tax credit so reversed must be provided in this row.

All Other Input Tax Credit Reversed

In case any other input tax credit is reversed for any other reason, details of such reversal can be provided in this row with break up of integrated tax, state tax, central tax and cess.

Net Input Tax Credit Availed

Based on the information provided above, net input tax credit available to the taxpayer is calculated automatically in row C.

Ineligible Input Tax Credit

Certain items like food, beverages, life insurance, health club memberships and more are ineligible for GST input tax credit. Details of such items that were not eligible for input tax credit must be mentioned in row D.

Step 4: Prepare Inward Supplies Exempt from GST

GSTR 3B Inward Supplies Exempt from GST

In this table, details of inward supplies that were exempt from GST must be provided.

In the first row, the total value of all supplies received from a composition scheme taxable person + purchases of goods or services that are exempted from GST + goods and services purchased with nil GST rate must be provided. The details must be divided between inter-state supplies and intra-state supplies.

In the second row, details of purchases of all non-GST goods and services must be mentioned, if any. For most taxpayers, this row would be nil.

Step 5: Prepare details of GST paid

GSTR 3B Payment of Tax

In this table, details of tax payable and GST tax paid must be provided by the taxpayer. The Government portal, auto-populates the tax payable based on the infromation provided in the previous tables. The total tax payable by the taxpayer can also be calculated by adding all integrated tax, central tax, state tax and cess payable. From the total

From the total tax payable, the input tax credit available calculated in step 3 would be auto-populated on the GST portal. In case the taxpayer paid any GST, then details of such taxpayment can be provided in column 8. Interest and late fee would be zero if GSTR 3B if filed on time with GST payment.

Step 6: Details of TDS and TCS

GSTR 3B TDS & TCS Credit

In this table, the input has been disabled on the GST portal as TDS and TCS provisions have not come into effect. Hence, taxpayers need not worry about calculating TDS or TCS for the GSTR 3B return to be filed in August.

Step 7: Filing GSTR 3B on GST Portal

Once the above details are prepared manually or through a GST software, GSTR 3B return can be filed on the GST portal within a few minutes. In case you use LEDGERS GST software, we will calculate all of the information above based on the invoices and purchase invoices you had generated. Hence, you can simply enter the information provided by us into the GST Portal and click on submit.

In case you do not use LEDGERS, you would have to prepare the above information manually to file the same on the GST portal.

LEDGERS GST Software

Using LEDGERS GST software you can prepare and file GSTR 3B return in a few clicks. In case you are not using LEDGERS GST Software, you can follow the steps below to calculate and file GSTR 3B return.

Export supplies of a taxpayer registered under GST are classified as zero rated supply. Zero rated supply under GST is eligible for refund. Taxpayers are required to furnish details of all zero rated supply in GSTR 3B return and GSTR 1 return.

What is Zero Rated Supply?

GST is not applicable in India for exports. Hence, all export supplies of a taxpayer registered under GST would be classified as zero rated supply. According to Section 16 of the IGST Act, zero rated supply means any of the following supplies of goods or services:

Export of goods or services or both;

Supply of goods or services or both to a Special Economic Zone developer

Supply of goods or services or both to a Special Economic Zone unit.

GST Refund for Zero Rated Supply

As exports are zero rated supply, the supplier will be eligible to claim input tax credit in respect of goods or services used for the supplies even though they might be non-taxable or even exempt supplies.

To claim GST refund for exports, the taxpayer can export under bond or LUT and claim refund or export on payment of IGST and claim refund.

Details to be Furnished in GST Returns

In GSTR 3B return and GSTR-1, all taxpayers must furnish details of all zero rated supply. In the following table showing GSTR 3B return, the taxpayer must provide details of all export supply in row B.

GSTR 3B Details of Outward Supplies

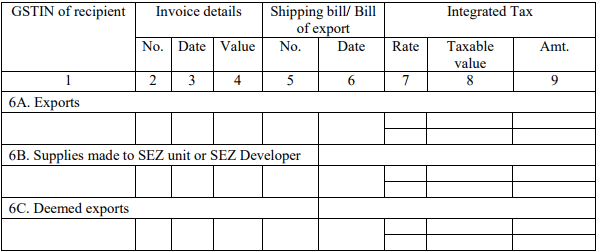

In GSTR-1 return, details of all export supply must be provided under the categories of exports, supplies made to SEZ unit or SEZ Developer and deemed exports.

GSTR-1 Zero rated supplies

Zero Rated vs Exempt Supply

Export and supplies to SEZ units or developers are classified as zero rated supply. On the other hand, nil or exempt supply are those supply with 0% GST rate.

Under GST, a refund can be claimed by taxpayer for any tax and interest paid or any other amount of GST by making an application for GST refund before 2 years from the relevant date. In this article, we look at the procedure for obtaining GST refund and refund of unutilised input tax credit under GST in detail.

Refund of Unutilised Input Tax Credit

Input tax credit mechanism in GST ensures that GST liability is ultimately passed on to the end consumer of a goods or service. However, throughout the value chain, every person is required to pay GST and then claim input tax credit on GST paid to reduce GST liability. In such a scenario, it is possible for some taxpayers to accumulate input tax credit that cannot be set off against GST liability.

In such a scenario, it is possible for some taxpayers to accumulate input tax credit that cannot be set off against GST liability. Hence, the GST Act provides a procedure for applying for a refund of unutilised input tax credit. According to the GST Act, only the following of unutilised input tax credit will be eligible for a refund:

Zero rated supplies made without payment of tax;

Input tax credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies).

It is important to note that the Act does not allow refund of unutilised input tax credit where the goods exported out of India are subjected to export duty. Also, no refund of input tax credit is allowed, if the supplier of goods or services or both avails of drawback in respect of central tax or claims refund of the integrated tax paid on such supplies.

GST Refund for Zero Rated Supply

In case of zero rated supply without payment of tax under bond or letter of undertaking, refund of input tax credit is calculated based on the following formula

Refund Amount = (Turnover of zero-rated supply of goods + Turnover of zero-rated supply of services) x Net ITC ÷Adjusted Total Turnover

“Refund amount” means the maximum refund that is admissible.

“Net ITC” means input tax credit availed on inputs and input services during the relevant period.

“Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking.

“Turnover of zero-rated supply of services” means the value of zero-rated supply of services made without payment of tax under bond or letter of undertaking.

“Adjusted Total turnover” means the turnover in a State or a Union territory, as defined under sub-section (112) of section 2, excluding the value of exempt supplies other than zero-rated supplies, during the relevant period.

“Relevant period” means the period for which the claim has been filed.

GST Refund Due to Inverted Duty Structure

In the case of refund on account of inverted duty structure, refund of unutlised input tax credit is granted based on the following formula:

Maximum Refund Amount = {(Turnover of inverted rated supply of goods) x Net ITC ÷ Adjusted Total Turnover} – tax payable on such inverted rated supply of goods

Applying for Refund of Unutilised Input Tax Credit

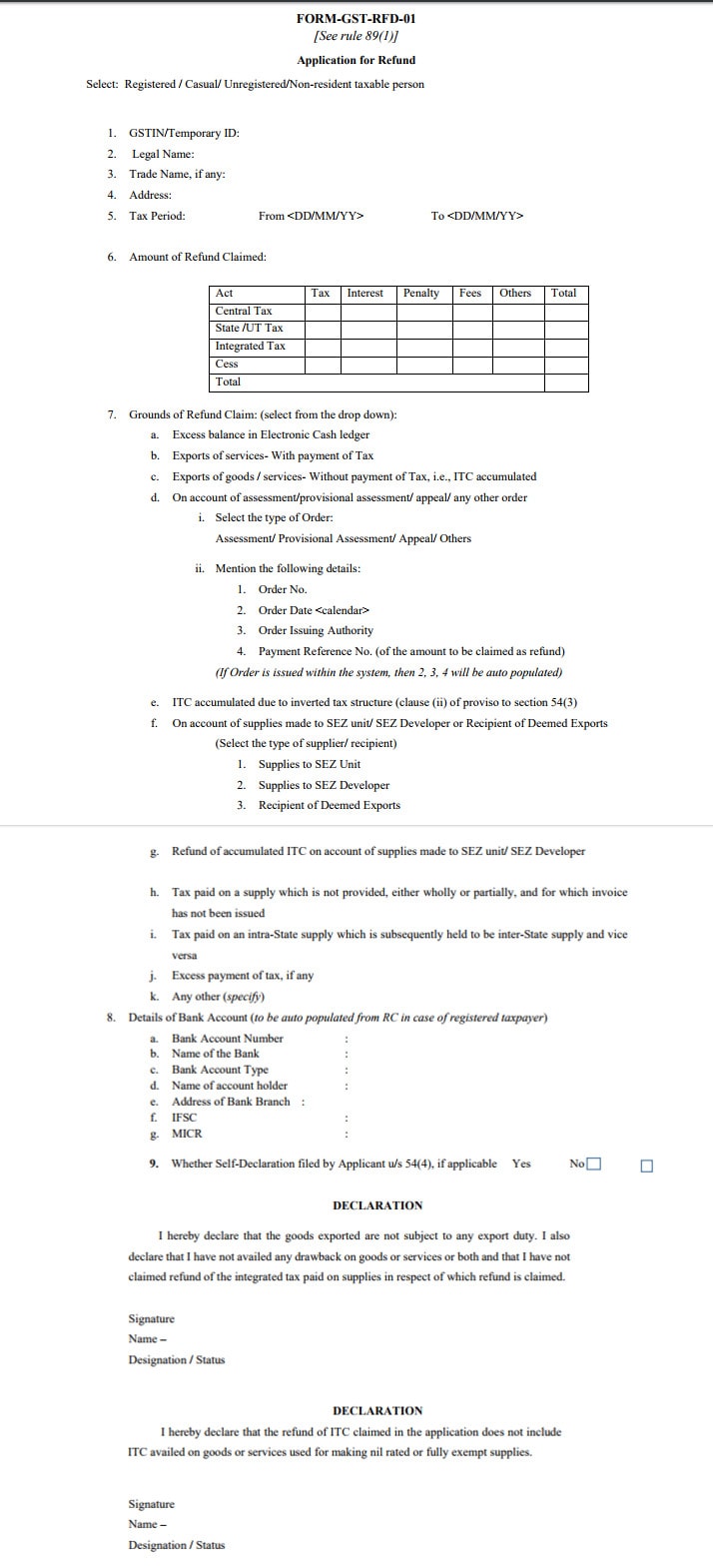

An application for refund of unutlised input tax credit must be submitted in Form GST RFD-01 as shown below:

GST Refund Application Form

Along with the GST refund application form, the taxpayer must submit documentary evidence supporting the GST refund. In case the GST refund claimed is less than Rs.2 lakhs, then the taxpayer can submit a declaration instead of submitting documentary evidences.

If the GST refund claimed is over Rs.2 lakhs, then documentary evidence must be submitted mandatorily. Based on the type of GST refund claim, one or more fo the following documents must be submitted as evidence.

Reference number of the order and a copy of the order passed by the proper officer or an appellate authority or Appellate Tribunal or court resulting in such refund or reference number of the payment of the amount specified in sub-section (6) of section 107 and sub-section (8) of section 112 claimed as refund.

Statement containing the number and date of shipping bills or bills of export and the number and the date of the relevant export invoices, in a case where the refund is on account of export of goods.

Statement containing the number and date of invoices and the relevant Bank Realisation Certificates or Foreign Inward Remittance Certificates, as the case may be, in a case where the refund is on account of the export of services.

Statement containing the number and date of invoices as provided in rule 46 along with the evidence regarding the endorsement specified in the second proviso to sub-rule (1) in the case of the supply of goods made to a Special Economic Zone unit or a Special Economic Zone developer.

Statement containing the number and date of invoices, the evidence regarding the endorsement specified in the second proviso to sub-rule (1) and the details of payment, along with the proof thereof, made by the recipient to the supplier for authorised operations as defined under the Special Economic Zone Act, 2005, in a case where the refund is on account of supply of services made to a Special Economic Zone unit or a Special Economic Zone developer.

Declaration to the effect that the Special Economic Zone unit or the Special Economic Zone developer has not availed the input tax credit of the tax paid by the supplier of goods or services or both, in a case where the refund is on account of supply of goods or services made to a Special Economic Zone unit or a Special Economic Zone developer;

Statement containing the number and date of invoices along with such other evidence as may be notified in this behalf, in a case where the refund is on account of deemed exports.

Statement containing the number and the date of the invoices received and issued during a tax period in a case where the claim pertains to refund of any unutilised input tax credit under sub-section (3) of section 54 where the credit has accumulated on account of the rate of tax on the inputs being higher than the rate of tax on output supplies, other than nil-rated or fully exempt supplies;.

Reference number of the final assessment order and a copy of the said order in a case where the refund arises on account of the finalisation of provisional assessment.

Statement showing the details of transactions considered as intra-State supply but which is subsequently held to be inter-State supply.

Statement showing the details of the amount of claim on account of excess payment of tax.

Declaration to the effect that the incidence of tax, interest or any other amount claimed as refund has not been passed on to any other person, in a case where the amount of refund claimed does not exceed two lakh rupees.

Certificate in Annexure 2 of FORM GST RFD-01 issued by a chartered accountant or a cost accountant to the effect that the incidence of tax, interest or any other amount claimed as refund has not been passed on to any other person, in a case where the amount of refund claimed exceeds two lakh rupees:

The GST Act, has explicitly mentioned that renting of immovable property would be treated as supply of services. However, GST is applicable only on certain types of rent. In this article, we look at types of rent that attract GST in India.

Renting of Immovable Property

In Schedule 2 of the GST Act, the following types of transactions with respect to land and building have been defined as supply of services.

Any lease, tenancy, easement, licence to occupy land is a supply of services;

Any lease or letting out of the building including a commercial, industrial or residential complex for business or commerce, either wholly or partly, is a supply of services.

However, services by way of renting of residential dwelling for use as residence is exempt from GST. Hence, only renting of residential premises for use as residence is exempt from GST.

Any other type of lease or letting out of immovable property (even if it is a residential properly) for business or commerce would be treated as a supply of service attracting GST at 18% rate. The key to

Thus, the key to determining if GST is applicable for renting of immovable property is whether the property would be used for business or commerce. If the property would be used for business, then GST would be applicable on the rent at 18%.

GST on Rent a Cab

Under service tax regulation, metered cabs or auto rickshaws (including E-rickshaws) were exempt from service tax. The GST Council has decided to extend the same exemption under GST. Hence, GST is not applicable for metered cabs or auto rickshaws.

GST on Renting of Commercial Premises

Under GST, renting of precincts of a religious place meant for general public, owned or managed by an entity registered as a charitable or religious trust or a trust or an institution or a body or an authority is exempt from GST as follows:

Renting of rooms where charges are Rs 1000/- or less per day.

Renting of premises, community halls, kalyanmandapam or open area, etc where charges are Rs 10,000/- or less per day.

Renting of shops or other spaces for business or commerce where charges are Rs 10,000/-or less per month

In all other cases, GST at the rate of 18% would be applicable on the taxable value and the rental would be treated as a taxable supply of service.

Credit notes are a type of business document issued by a seller usually when goods are returned by a customer. Under GST, specific rules have been provided for the issue of credit note along with credit note format. In this article, we look at credit notes under GST in detail.

When credit note is issued?

A credit note can be issued after a tax invoice when the taxable value and tax charged in the invoice is more than the taxable value or tax chargeable for the supply. Hence, the following are instances when a taxpayer can issue a credit note to the customer:

When tax invoice is found to exceed the value of supply

When goods are returned by the customer

When goods are found to be deficient

Credit Note vs Debit Note

A debit note is issued after a tax invoice when the taxable value or tax charged in the invoice is found to be less than the value payable by the customer. On the other hand, a credit note is issued when the taxable value in the invoice is more than the taxable value chargeable for the supply. In simple terms:

If Invoice Value > Amount Due from Customer – Issue Credit Note

If Amount Due from Customer > Invoice Value – Issue Debit Note

What is the procedure for issuing credit note under GST?

The GST Rules provide a specific format for credit notes as under:

Name, address and Goods and Services Tax Identification Number of the taxpayer.

Nature of the document. (Credit or Debit Note)

Consecutive serial number not exceeding sixteen characters, in one or multiple series.

Date of issue of credit note.

Name, address and GSTIN or UIN of the customer, if registered.

Name and address of the recipient and the address of delivery, along with the name of State and its code, if recipient is un-registered.

Serial number and date of the related tax invoice or bill of supply.

Value of taxable supply of goods or services, rate of tax and the amount of the tax credited.

Signature or digital signature of the supplier or his authorised representative.

Details of Credit Note to be Filed in GST Returns

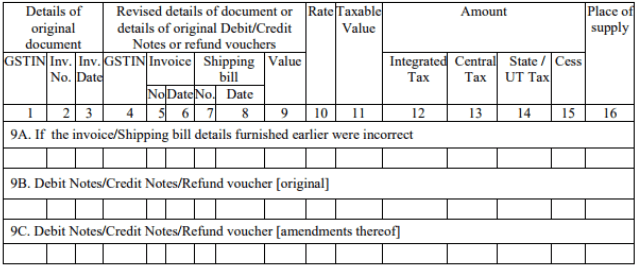

In GSTR 1 Filing, all taxpayers are required to provide details of all credit notes or debit notes issued by them during the previous month in the following format

GSTR 1 Amendments to taxable supplies

The details of credit notes issued and credit notes amended during the previous month must be provided along with the details of original invoice number, invoice date and GSTIN of the customer. All credit notes pertaining to a financial year must be issued and filed no later than September following the end of financial year or the date of filing of GST annual return, whichever is earlier. Based on the credit notes issued by the taxpayer, the tax liability would be adjusted. However, no reduction in output tax liability of the taxpayer is permitted, if the incidence of tax and interest on such supply has been passed onto any other person.

GSTR 3B Details of Outward Supplies

GSTR 3B Details of Outward Supplies